Snowball vs. Avalanche Method: What’s Best for You?

Snowball vs. Avalanche Method: What’s Best for You?

Jan 24, 2025

Debt can feel overwhelming, but having a structured repayment strategy can make all the difference.

Two of the most popular debt reduction methods are the snowball and avalanche methods. Each has its pros and cons, so understanding them will help you decide which strategy aligns with your financial goals.

If you're wondering how to quickly get out of debt, this guide will break down both approaches to help you choose the best one for your situation.

What is the Debt Snowball Method?

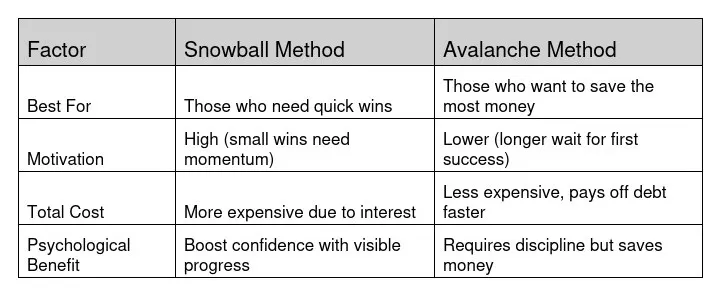

The debt snowball method focuses on paying off the smallest debt first while making minimum payments on all others. Once the smallest debt is eliminated, you roll that payment into the next smallest debt, creating a “snowball effect.”

How It Works:

List your debts from smallest to largest (regardless of interest rate).

Make the minimum payment on all debts except the smallest.

Put as much extra money as possible toward the smallest debt.

Once paid off, apply that total payment to the next smallest debt.

Repeat until all debts are eliminated.

Pros:

✅ Provides quick wins that boost motivation.

✅ Keeps momentum going, making it easier to stay on track.

✅ Best for those who need psychological encouragement.

Cons:

❌ May result in paying more interest over time.

❌ Doesn't prioritize high-interest debts, which can be costly.

What is the Debt Avalanche Method?

The debt avalanche method prioritizes debts with the highest interest rates first, minimizing the total amount paid over time.

How It Works:

List your debts from highest to lowest interest rate.

Make minimum payments on all debts except the one with the highest interest.

Allocate all extra funds toward the highest-interest debt.

Once paid off, roll that payment into the next highest-interest debt.

Repeat until all debts are gone.

Pros:

✅ Saves the most money on interest over time.

✅ Helps pay off debt faster if you stay disciplined.

✅ Best for those focused on minimizing long-term costs.

Cons:

❌ Takes longer to see results, which can reduce motivation.

❌ Requires strong financial discipline to stay committed.

Snowball vs. Avalanche: Which One is Right for You?

Choosing between the two methods depends on your personality, financial habits, and what keeps you motivated.

How to Quickly Get Out of Debt Using Either Method

Regardless of which strategy you choose, these tips will help accelerate your debt payoff:

✔ Create a Budget: Track your income and expenses to maximize extra payments toward debt.

✔ Cut Unnecessary Spending: Reduce discretionary spending and put the savings toward your debt.

✔ Increase Your Income: Consider side hustles or freelance work to generate additional payments.

✔ Negotiate Lower Interest Rates: Call creditors to request lower rates or look into balance transfer options.

✔ Stay Consistent: Commit to your strategy and avoid accumulating new debt.

Conclusion

Both the snowball and avalanche methods are effective debt reduction strategies, but the right choice depends on your personal preferences. If you need quick motivation, go with the snowball method. If you want to save the most money in the long run, the avalanche method is best.

No matter which method you choose, the key to success is staying committed and making consistent payments.

Ready to tackle your debt? Pick a method and start today—your future self will thank you!