How to Negotiate Credit Card Debt and Take Control of Your Finances

How to Negotiate Credit Card Debt and Take Control of Your Finances

Jan 21, 2025

If you're struggling with credit card debt, you’re not alone. Many people find themselves overwhelmed by high interest rates and minimum payments that barely make a dent.

But did you know that you can negotiate with your creditors to lower your payments, reduce interest rates, or even settle for less than what you owe?

Here’s how to negotiate credit card debt effectively and regain financial stability.

1. Understand Your Debt Situation

Before negotiating, gather all relevant details about your debt, including:

- Total balance owed

- Interest rates

- Minimum monthly payments

- Late fees and penalties

- Your current financial situation (income, expenses, and other debts)

Creditors will ask for this information, so having it prepared will make negotiations smoother.

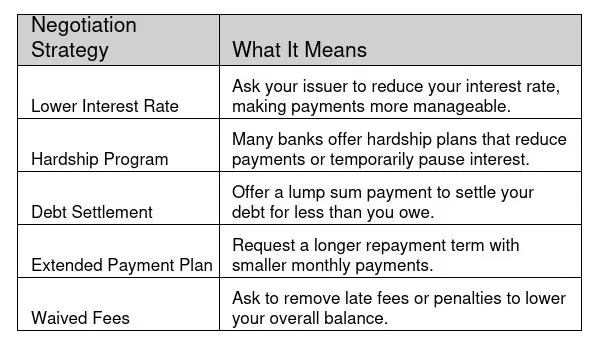

2. Know Your Options Before Calling

When negotiating, you have several options to explore:

3. How to Approach the Negotiation

Step 1: Contact Your Credit Card Issuer

Call your creditor’s customer service number and ask to speak with the hardship department or a debt specialist. Be polite, but firm about your request.

Step 2: Explain Your Situation Clearly

Tell them why you’re struggling to make payments. If you lost your job, had a medical emergency, or faced unexpected financial hardship, let them know.

Step 3: Make a Reasonable Offer

If negotiating a settlement, start low but reasonable—for example, offering 30-50% of the total balance.

Step 4: Get Everything in Writing

Once an agreement is reached, request a written confirmation before making any payments.

4. What to Do If Creditors Won’t Budge

If negotiations fail, consider:

- Speaking with a supervisor – A higher-up may have more authority to approve your request.

- Trying again later – Some companies are more flexible after a few missed payments.

- Debt consolidation – Combining debts into one loan with a lower interest rate.

- Seeking professional help – A credit counseling service can negotiate on your behalf.

Key Takeaways

- Credit card debt is negotiable—creditors prefer partial payments over non-payment.

- Be prepared with financial details before calling your issuer.

- Ask for lower interest rates, waived fees, or payment extensions to ease your burden.

- Always get agreements in writing before making payments.

FAQs

1. Can I negotiate credit card debt on my own?

Yes! You don’t need a lawyer or debt relief service to negotiate. With the right approach, many creditors will work with you directly.

2. How much will credit card companies settle for?

It varies, but settlements typically range between 30% to 50% of the outstanding balance.

3. Does negotiating credit card debt hurt my credit score?

It depends. If you settle for less than you owe, it may impact your score. However, making a new payment plan or reducing interest rates can help avoid missed payments.

4. What should I do if a creditor refuses to negotiate?

Try calling again, speaking to a supervisor, or exploring debt consolidation or credit counseling options.

5. Are there fees for negotiating credit card debt?

If you do it yourself, no. But third-party debt settlement companies may charge fees, so be cautious before using them.

Conclusion

Negotiating credit card debt may seem daunting, but with the right approach, it can lead to real financial relief. Being proactive, prepared, and persistent is key.

Creditors are often willing to work with you, but you need to initiate the conversation. Start by assessing your financial situation, knowing your options, and making a strategic call to your credit card issuer.

If one method doesn’t work, don’t get discouraged—explore other strategies like speaking with a supervisor, trying again later, or seeking professional advice. The most important thing is to take action and not ignore your debt. The sooner you start negotiating, the sooner you can create a repayment plan that works for you and regain financial stability.

Take control today, make that call, and start paving the way toward a debt-free future!